“Master Your Money: The 50/30/20 Budget Rule Explained!”

Understanding the 50/30/20 Budget Rule: A Simple Guide to Managing Your Finances

The 50/30/20 budget rule is a straightforward yet effective approach to managing personal finances. It provides a clear framework for allocating income into three distinct categories: needs, wants, and savings. By following this method, individuals can develop better financial habits, ensure essential expenses are covered, and work toward long-term financial goals. Understanding how this rule works and whether it suits your financial situation is crucial for making informed decisions about budgeting and money management.

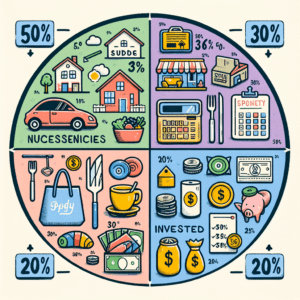

At its core, the 50/30/20 rule divides after-tax income into three primary categories. The first category, which accounts for 50% of income, is dedicated to needs. These are essential expenses that are necessary for daily living, such as housing, utilities, groceries, transportation, insurance, and minimum debt payments. Since these expenses are non-negotiable, ensuring they do not exceed half of one’s income helps maintain financial stability. If essential costs surpass this threshold, it may be necessary to reassess spending habits or explore ways to increase income.

The second category, comprising 30% of income, is allocated to wants. Unlike needs, wants are discretionary expenses that enhance quality of life but are not essential for survival. This category includes dining out, entertainment, travel, hobbies, and subscription services. While these expenses contribute to personal enjoyment, maintaining a balance is important to avoid overspending. By setting a clear limit on discretionary spending, individuals can indulge in non-essential purchases without compromising financial security.

The final 20% of income is designated for savings and debt repayment beyond minimum payments. This portion is crucial for building financial security and preparing for the future. It includes contributions to emergency funds, retirement accounts, investments, and additional payments toward outstanding debts. Prioritizing savings ensures that individuals are prepared for unexpected expenses and can work toward long-term financial goals, such as homeownership or early retirement. By consistently setting aside a portion of income for savings, financial stability becomes more attainable over time.

While the 50/30/20 rule provides a simple and effective budgeting framework, it may not be suitable for everyone. Individual financial situations vary based on income level, cost of living, and personal financial goals. For instance, those living in high-cost areas may find it challenging to keep essential expenses within 50% of their income. Similarly, individuals with significant debt may need to allocate more than 20% toward repayment to achieve financial freedom sooner. In such cases, adjusting the percentages to better fit personal circumstances can make the budgeting method more practical.

Additionally, those with irregular income, such as freelancers or gig workers, may need to modify the rule to accommodate fluctuating earnings. Establishing a baseline budget based on average income and prioritizing savings during higher-earning months can help maintain financial stability. The key is to use the 50/30/20 rule as a guideline rather than a rigid formula, making adjustments as needed to align with individual financial goals.

Ultimately, the effectiveness of the 50/30/20 budget rule depends on personal financial priorities and circumstances. By understanding its principles and adapting them as necessary, individuals can create a structured approach to managing their finances. Whether used as a starting point or a long-term strategy, this budgeting method offers a practical way to balance essential expenses, discretionary spending, and savings, leading to greater financial security and peace of mind.

Pros and Cons of the 50/30/20 Budget Rule: Is It the Right Fit for You?

The 50/30/20 budget rule is a widely recognized framework for managing personal finances, offering a straightforward approach to allocating income. By dividing after-tax earnings into three categories—50% for needs, 30% for wants, and 20% for savings and debt repayment—this method provides a structured way to balance financial priorities. However, while it offers simplicity and clarity, it may not be suitable for everyone. Understanding the advantages and limitations of this budgeting strategy can help determine whether it aligns with individual financial goals and circumstances.

One of the primary benefits of the 50/30/20 rule is its simplicity. Unlike more complex budgeting methods that require meticulous tracking of every expense, this approach provides clear guidelines that are easy to follow. By categorizing expenses into broad groups, individuals can quickly assess whether they are maintaining a balanced financial plan. This simplicity makes it particularly appealing to those who are new to budgeting or prefer a less time-consuming method of managing their finances.

Another advantage is its flexibility. The 50/30/20 rule does not impose rigid spending limits on specific categories but instead allows individuals to adjust their expenses within the three main divisions. This flexibility enables people to prioritize their financial needs while still allocating funds for discretionary spending and long-term savings. Additionally, by ensuring that 20% of income is dedicated to savings and debt repayment, this method encourages financial stability and long-term wealth accumulation.

However, despite its benefits, the 50/30/20 rule may not be suitable for everyone. One of its main limitations is that it assumes a relatively stable income and cost of living. For individuals living in high-cost areas, allocating only 50% of income to necessities such as housing, utilities, and transportation may be unrealistic. In such cases, essential expenses may consume a larger portion of income, leaving less room for discretionary spending and savings. Similarly, those with lower incomes may struggle to meet their basic needs within the prescribed limits, making it difficult to adhere to this budgeting framework.

Another potential drawback is that the rule may not accommodate individuals with unique financial obligations. For example, those with significant debt may need to allocate more than 20% of their income toward repayment to achieve financial stability. Likewise, individuals with aggressive savings goals, such as early retirement or major investments, may find the 20% savings allocation insufficient. In such cases, a more customized budgeting approach may be necessary to align with specific financial objectives.

Furthermore, the 50/30/20 rule does not account for variations in financial priorities across different life stages. Young professionals may have different spending and saving needs compared to retirees or families with children. As financial responsibilities evolve, a rigid adherence to this rule may not always be practical. Adjusting the budget to reflect changing circumstances can be more effective in maintaining financial well-being over time.

Ultimately, while the 50/30/20 budget rule provides a useful framework for managing finances, its effectiveness depends on individual financial situations. Those with stable incomes and moderate living expenses may find it a helpful guide, while others may need to modify the allocations to better suit their needs. By evaluating personal financial goals and obligations, individuals can determine whether this budgeting method is the right fit or if an alternative approach would be more beneficial.

Adapting the 50/30/20 Budget Rule to Your Financial Goals and Lifestyle

The 50/30/20 budget rule provides a simple yet effective framework for managing personal finances, but its success depends on how well it aligns with an individual’s financial goals and lifestyle. While the rule suggests allocating 50% of income to needs, 30% to wants, and 20% to savings and debt repayment, personal circumstances may require adjustments to ensure financial stability and long-term success. Adapting this budgeting method to fit specific financial situations can help individuals maintain control over their money while still working toward their objectives.

One of the first considerations when applying the 50/30/20 rule is income level and cost of living. In high-cost areas, essential expenses such as housing, utilities, and transportation may exceed the recommended 50% allocation. In such cases, individuals may need to adjust their budget by reducing discretionary spending or finding ways to increase income. Conversely, those living in lower-cost areas may find that their essential expenses fall well below the 50% threshold, allowing them to allocate more funds toward savings or discretionary spending. By assessing personal financial circumstances, individuals can modify the rule to better reflect their needs.

Another important factor to consider is financial goals. While the 50/30/20 rule provides a balanced approach, some individuals may need to prioritize savings or debt repayment more aggressively. For example, those working toward early retirement or significant financial milestones may choose to allocate more than 20% of their income to savings and investments. Similarly, individuals with high-interest debt may benefit from dedicating a larger portion of their budget to debt repayment to reduce financial strain in the long run. Adjusting the percentages based on personal goals ensures that financial planning remains aligned with long-term aspirations.

Lifestyle choices also play a crucial role in determining how the 50/30/20 rule should be adapted. Some individuals may prioritize experiences, travel, or hobbies, making the 30% allocation for discretionary spending particularly important. Others may prefer a more frugal lifestyle, allowing them to redirect funds toward savings or investments. Understanding personal values and spending habits can help individuals make informed decisions about how to distribute their income while maintaining financial discipline.

Additionally, life stages and responsibilities influence how the budget should be structured. Young professionals just starting their careers may have different financial priorities than families with children or individuals nearing retirement. For instance, those in the early stages of their careers may focus on building an emergency fund and paying off student loans, while families may need to allocate more funds toward childcare and education expenses. Meanwhile, individuals approaching retirement may prioritize maximizing retirement contributions and reducing outstanding debts. Recognizing these differences allows for a more personalized approach to budgeting.

Ultimately, the 50/30/20 budget rule serves as a guideline rather than a rigid formula. While it provides a solid foundation for financial management, flexibility is key to ensuring that it meets individual needs. By evaluating income, financial goals, lifestyle preferences, and life stages, individuals can tailor the rule to create a budget that supports both short-term stability and long-term financial success. Making thoughtful adjustments ensures that financial planning remains practical, sustainable, and aligned with personal aspirations.