“Money-Saving Myths Exposed: Stop Wasting, Start Saving!”

**Skipping Regular Maintenance to Save Money**

Many people believe that skipping regular maintenance on their homes, vehicles, and appliances is a smart way to cut costs. At first glance, it may seem like avoiding routine check-ups and servicing can help save money, but in reality, this approach often leads to higher expenses in the long run. While it is tempting to delay maintenance to reduce immediate costs, neglecting essential upkeep can result in costly repairs, decreased efficiency, and even complete system failures.

One of the most common areas where people try to save money by avoiding maintenance is with their vehicles. Regular oil changes, tire rotations, and brake inspections may seem like unnecessary expenses, but they play a crucial role in keeping a car running smoothly. When these routine services are ignored, minor issues can escalate into major mechanical failures. For example, failing to change the oil regularly can lead to engine damage, which is significantly more expensive to repair than the cost of routine oil changes. Similarly, neglecting tire maintenance can result in uneven wear, reducing fuel efficiency and increasing the likelihood of a blowout, which could lead to costly repairs or even accidents.

The same principle applies to home maintenance. Many homeowners put off servicing their HVAC systems, plumbing, and roofing in an effort to save money. However, small issues that go unnoticed or unaddressed can quickly turn into expensive problems. A minor leak in a pipe, for instance, may seem insignificant at first, but over time, it can cause water damage, mold growth, and structural issues that require extensive repairs. Likewise, failing to clean and maintain an HVAC system can lead to reduced efficiency, higher energy bills, and costly breakdowns. By investing in regular maintenance, homeowners can prevent these problems and extend the lifespan of their systems, ultimately saving money in the long term.

Appliances are another area where skipping maintenance can be a costly mistake. Many people assume that as long as an appliance is functioning, there is no need for upkeep. However, neglecting tasks such as cleaning refrigerator coils, descaling a water heater, or servicing a washing machine can lead to decreased efficiency and premature failure. A refrigerator with dirty coils, for example, has to work harder to maintain the desired temperature, leading to higher energy consumption and a shorter lifespan. Similarly, a water heater that is not regularly flushed can accumulate sediment, reducing its efficiency and increasing the risk of breakdowns. By performing routine maintenance, homeowners can ensure that their appliances operate efficiently and last longer, reducing the need for costly replacements.

Beyond the financial implications, skipping regular maintenance can also pose safety risks. A poorly maintained vehicle is more likely to experience mechanical failures that could lead to accidents. Likewise, neglected home systems, such as faulty electrical wiring or a malfunctioning furnace, can create fire hazards or carbon monoxide leaks. By staying proactive with maintenance, individuals can not only save money but also protect their safety and well-being.

Ultimately, while it may seem like skipping regular maintenance is a way to cut costs, the reality is that it often leads to greater expenses down the line. Investing in routine upkeep helps prevent costly repairs, improves efficiency, and extends the lifespan of valuable assets. By prioritizing maintenance, individuals can avoid unnecessary financial burdens and ensure that their homes, vehicles, and appliances remain in optimal condition for years to come.

**Buying Cheap Instead of Investing in Quality**

Many people believe that buying the cheapest option available is the best way to save money. At first glance, this approach seems logical—spending less upfront means keeping more money in your pocket. However, this common belief often leads to higher costs in the long run. While it may seem counterintuitive, choosing inexpensive products over high-quality alternatives can result in frequent replacements, increased maintenance expenses, and even potential safety risks. Understanding the hidden costs of buying cheap instead of investing in quality is essential for making smarter financial decisions.

One of the most significant drawbacks of purchasing low-cost items is their lack of durability. Manufacturers of inexpensive products often use lower-quality materials and less precise craftsmanship to keep production costs down. As a result, these items tend to wear out or break much faster than their higher-quality counterparts. For example, a cheaply made pair of shoes may seem like a bargain at first, but if they fall apart within a few months, replacing them repeatedly will ultimately cost more than investing in a well-made pair that lasts for years. The same principle applies to household appliances, furniture, and even clothing—opting for quality from the start can prevent the need for frequent replacements.

Beyond durability, another hidden cost of buying cheap is the potential for increased maintenance and repair expenses. Lower-quality products often require more frequent servicing, which can quickly add up over time. Consider a budget-friendly car with a lower initial price tag but a reputation for mechanical issues. While the upfront savings may be appealing, ongoing repairs and maintenance costs can quickly surpass the price of a more reliable vehicle. Similarly, inexpensive home appliances may break down more often, leading to costly repairs or even premature replacement. In contrast, investing in well-made products with strong warranties and reliable performance can reduce long-term expenses and provide greater peace of mind.

In addition to financial concerns, buying cheap can also have safety implications. Many low-cost products are manufactured with minimal quality control, which can lead to defects or safety hazards. Electrical appliances, for instance, may not meet safety standards, increasing the risk of malfunctions or even fires. Similarly, inexpensive tools or equipment may not be built to withstand regular use, posing potential dangers to users. By prioritizing quality over price, consumers can ensure that the products they purchase meet safety standards and perform reliably over time.

Another often-overlooked consequence of choosing cheap over quality is the environmental impact. Low-cost products are frequently made with inferior materials that degrade quickly, leading to increased waste. Fast fashion, for example, encourages consumers to buy inexpensive clothing that wears out rapidly, contributing to excessive textile waste. In contrast, investing in well-made, sustainable products reduces waste and promotes responsible consumption. While the initial cost may be higher, the long-term benefits for both the consumer and the environment make quality a more cost-effective choice.

Ultimately, while it may be tempting to save money by purchasing the cheapest option available, this approach often leads to higher costs in the long run. Durability, maintenance expenses, safety concerns, and environmental impact all play a role in determining the true value of a purchase. By shifting the focus from short-term savings to long-term investment, consumers can make more informed financial decisions that lead to greater savings and overall satisfaction.

**Avoiding Insurance to Cut Costs**

Many people believe that avoiding insurance is a smart way to cut costs, assuming that the money saved on premiums can be better used elsewhere. While this approach may seem financially prudent in the short term, it often leads to greater expenses in the long run. Insurance serves as a financial safety net, protecting individuals from unexpected costs that could otherwise be devastating. Without adequate coverage, a single accident, illness, or disaster can result in overwhelming financial burdens that far exceed the cost of regular premiums.

One of the most common areas where people try to save money is health insurance. Some individuals opt to forgo coverage, believing that they are healthy enough to avoid medical expenses. However, medical emergencies are unpredictable, and even a minor injury or illness can lead to significant medical bills. Without insurance, the cost of hospital visits, diagnostic tests, and treatments can quickly accumulate, leaving individuals with debt that could take years to repay. Additionally, preventive care, which is often covered by insurance, helps detect health issues early, potentially reducing the need for expensive treatments later. By skipping insurance, individuals may delay seeking medical attention, leading to more severe health problems and higher costs in the future.

Similarly, avoiding auto insurance can be a costly mistake. While some drivers may feel confident in their ability to avoid accidents, they cannot control the actions of others on the road. Even a minor collision can result in expensive repairs, medical bills, and legal fees. Without insurance, these costs must be paid out of pocket, which can be financially crippling. Furthermore, many regions legally require drivers to carry at least a minimum level of auto insurance. Failing to comply with these regulations can lead to fines, license suspension, or even legal action, adding to the financial strain.

Homeowners and renters insurance is another area where people attempt to cut costs, often underestimating the potential risks. Natural disasters, theft, and accidents can cause significant property damage or loss, leaving individuals without the means to recover. Without insurance, replacing belongings or repairing structural damage can be prohibitively expensive. Additionally, liability coverage included in many home insurance policies protects against legal claims if someone is injured on the property. Without this protection, homeowners may face costly lawsuits that could jeopardize their financial stability.

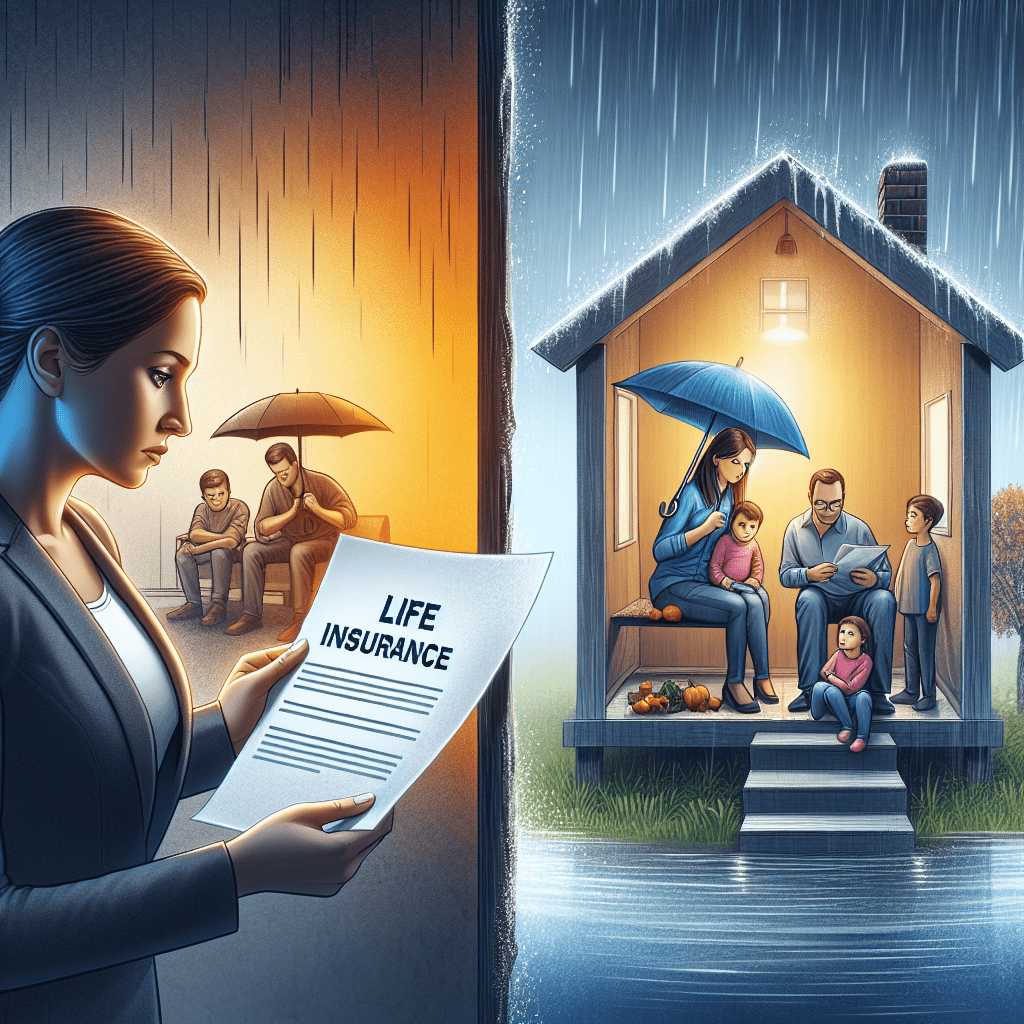

Life insurance is frequently overlooked, especially by younger individuals who believe they do not need it. However, life insurance provides financial security for loved ones in the event of an unexpected death. Without it, surviving family members may struggle to cover funeral expenses, outstanding debts, or daily living costs. While it may seem like an unnecessary expense, life insurance ensures that dependents are not left in financial distress.

Ultimately, avoiding insurance to save money is a risky strategy that often leads to greater financial hardship. While paying premiums may seem like an unnecessary expense, the protection that insurance provides far outweighs the potential costs of being uninsured. Instead of viewing insurance as an optional expense, it should be considered an essential component of financial planning. By maintaining adequate coverage, individuals can safeguard their financial well-being and avoid the devastating consequences of unexpected events.